The 1 July 2021 Superannuation Changes

Changes from 1 July 2021 will impact on how much money you can contribute to superannuation and how much you can have in your retirement phase superannuation account.

In general, your superannuation is either in an accumulation account (when you are building your super), a retirement account (when you meet preservation age and certain conditions of release and can withdraw your super), or in between when you are transitioning to retirement (when you reach perseveration age, are working reduced hours and take some of your superannuation as a pension).

The amount of money you can transfer from your accumulation account into your tax-free retirement account is limited by a transfer balance cap (TBC). From 1 July 2021, the current $1.6m general TBC will be indexed to $1.7m and once indexed, no single cap will apply to all individuals (each person will have an individual TBC between $1.6m and $1.7m).

Indexation will also change other superannuation caps and limits including:

Non-concessional contributions (contributions from after tax income)

Concessional contributions (contributions from before tax income such as super guarantee, salary sacrificed super amounts, or contributions you make and claim a tax deduction for etc.)

Co-contributions (personal contributions made by low and middle income earners matched by the Government up to $500), and

Contributions you make on behalf of your spouse that are eligible for a tax-offset.

How will the transfer balance cap impact me?

You are accumulating super

If you are building your superannuation (accumulation phase) and not withdrawing it*, indexation of the TBC is a good thing because from 1 July 2021 you will be able to access more of your superannuation tax-free. If you start taking your superannuation after 1 July 2021, for example if you meet a condition of release and retire, your transfer balance cap will be $1.7m. Essentially, if you have never had a transfer balance account credit, then the full indexation is available to you.

For low and middle income earners claiming the government co-contribution, the limit will increase in line with indexation to $1.7m.

Similarly, if you are contributing superannuation to your spouse and claiming the tax offset, the limit will increase in line with indexation to $1.7m. That is, you can contribute to your spouse’s superannuation and claim the tax offset as long as their TBC is not more than $1.7m.

You have started taking your super

If you started taking your superannuation before 1 July 2021 and have already had a credit added to your transfer balance account, then your TBC will be between $1.6m and $1.7m depending on the balance of your transfer balance account between 1 July 2017 and 30 June 2021. If your account reached $1.6m or more at any point during this time, your TBC after 1 July 2017 will remain at $1.6m. If the highest credit ever in your account was between $1 and $1.6m, then your TBC will be proportionally indexed based on the highest ever credit balance your transfer balance account reached. That is, the ATO will look at the highest amount your transfer balance account has ever been, then apply indexation to the unused cap amount. For example, if you started a retirement phase income stream valued at $1.2m on 1 October 2018 and this was the highest point of your account before 1 July 2021, then your unused cap is $400,000. This unused cap amount is used to work out your unused cap percentage (400k/1.6m=25%). The unused cap percentage is then applied to $100,000 ($100k*25%=$25k) to create your new TBC of $1,625,000.

Note that indexation only applies to the difference between the $1.6m TBC and the highest point of your account at any point between 1 July 2017 and 30 June 2021, not the value of your account at 30 June 2021. That is, if you made additional contributions after 1 October 2018 that increased your account to say $1,440,000, then indexation would apply to your unused cap of $160,000 (instead of $400,000), creating a TBC on 1 July 2021 of $1,610,000.

Indexation does not impact existing child death benefit beneficiaries. Child death benefit income streams commencing after 1 July 2021 will be entitled to the increment if the parent never had a transfer balance account or a proportion if the parent had a transfer balance account.

If you receive income from a capped defined benefit income stream and you are 60 years of age or more, or the income stream is from a death benefit where the member was over 60 at the time of death, then the defined benefit income cap will increase to $106,250 for most individuals. This will mean that the money your fund withholds from your income stream may change.

The amount you can contribute to super will increase

Indexation will increase the concessional and non-concessional contribution caps from 1 July 2021. These caps are indexed by average weekly ordinary time earnings (AWOTE).

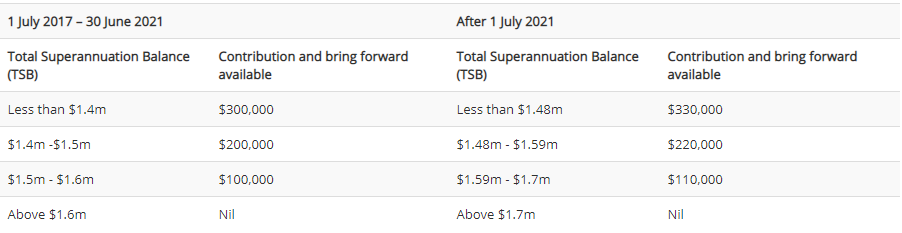

The bring forward rule

The bring forward rule enables you to contribute up to three years’ worth of non-concessional contributions in the one year. That is, from 1 July 2021, you could contribute up to $330,000 to your superannuation in one year. You can use the bring forward rule if you are 64 or younger on 1 July of the relevant financial year of the contribution and the contribution will not increase your total super balance by more than your transfer balance account cap.

If you utilised the bring forward rule in previous years, your non-concessional cap will not change. You will need to wait until your three years has expired before utilising the new cap limit.

* excludes withdrawals made under the COVID 19 relief measures.

Note: The material and contents provided in this publication are informative in nature only. It is not intended to be advice and you should not act specifically on the basis of this information alone. If expert assistance is required, professional advice should be obtained.